If the accumulation is justified to be within the reasonable needs of the business, the iaet is not imposed. What is corporate accumulated earnings tax when a corporation accumulates earnings without a reasonable business need and does not distribute out dividends to its shareholders, the corporation may be liable for the accumulated earnings tax in addition to its regular corporate income tax.

Cares Act Implications On Corporate Earnings And Profits Ep

The umbrella principle is simple:

Accumulated earnings tax reasonable business needs. Compute falco's accumulated earnings tax assuming that it had. However, this opens the door to the accumulated earnings tax (aet) if profits accumulate beyond the reasonable needs of the business. A corporation that permits the accumulation of earnings and profits beyond the reasonable needs of the business is subject to the 10 percent improperly accumulated earnings tax (iaet).

The accumulated earnings tax rate is 20 percent of accumulated taxable income. Determination of reasonable needs of the business. The threshold is $25000 without accumulated earning tax.

According to the irs, anything above this considered beyond the reasonable needs of the business. Assume that for these years at issue, a corporation is exempt up to $250,000 of accumulated earnings without demonstrating a reasonable business need for the accumulation. Preventing accumulations beyond reasonable needs the accumulated earnings tax was enacted to prevent a corporation from retaining earnings beyond its reasonable needs, instead of distributing earnings to sharehold.

To be subject to the accumulated earnings tax, the corporation generally must accumulate earnings beyond its reasonable business needs. And profits have been allowed to accumulate beyond the reasonable. The aet is only a tax on ati (undistributed current year earnings less dividend paid deduction in excess of aec).

The federal government discourages companies from “stockpiling” their capital by using the accumulated earnings tax. The aet is a penalty tax imposed on corporations for unreasonably accumulating earnings. A corporation that has an accumulation of earnings may be liable to pay the accumulated earnings tax unless the business can show that the earnings over the threshold are for reasonable needs of.

When applicable, the accumulated earnings tax is levied at the rate of 27y, percent of the first $100,000 of accumulated taxable income, and at. The accumulation of reasonable amounts for the payment of reasonably anticipated product liability losses (as defined in section 172(f) (as in effect before the date of enactment of the tax cuts and jobs act)), as determined under regulations prescribed by the secretary, shall be treated as accumulated for the reasonably anticipated needs of the business. Percent of the accumulated taxable income in excess of

The tax rate on accumulated earnings is 20%, the maximum rate at which they would be taxed if distributed. Reasonable needs of the business, the 10% improperly accumulated earnings tax shall be imposed. However, the undistributed prior year earnings still factor into the calculation of whether total accumulated earnings exceed the accumulated earnings credit or reasonable business needs.

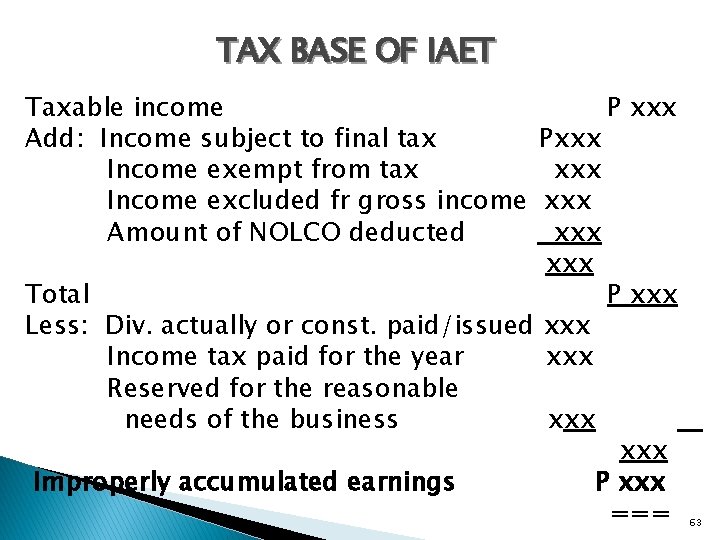

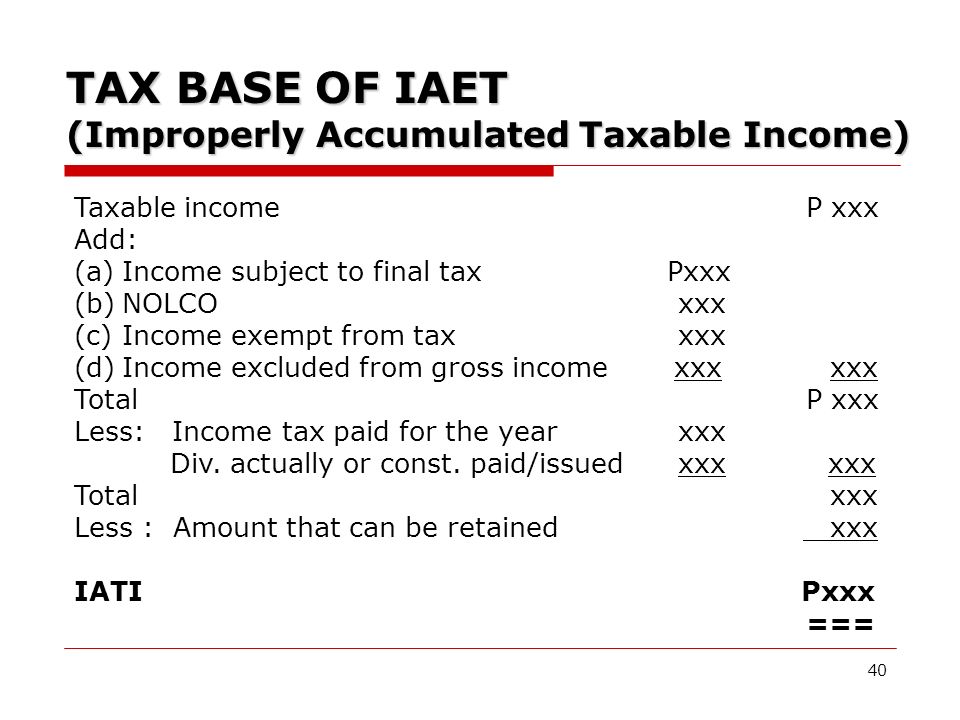

The mechanism imposing the accumulated earnings tax. A corporation that permits the accumulation of earnings and profits beyond the reasonable needs of the business is subject to the 10 percent improperly accumulated earnings tax (iaet). Accumulated taxable income is taxable income with adjustments, minus the dividends paid deduction and the accumulated earnings credit.

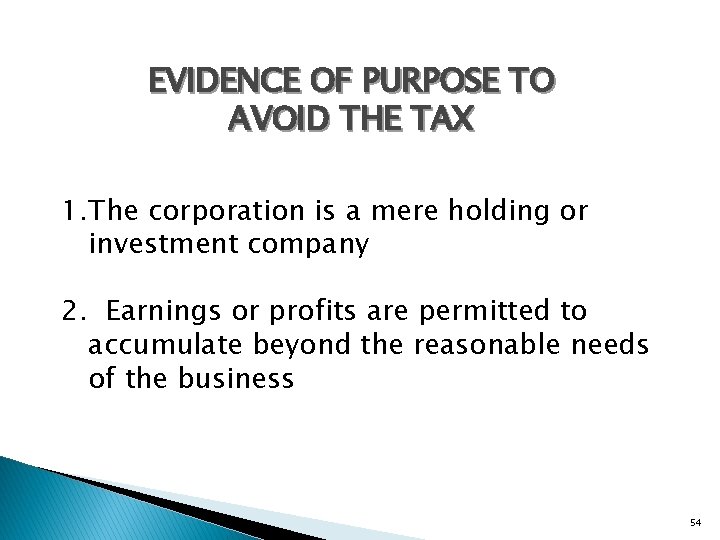

A corporation’s accumulation of earnings and profits beyond its reasonable business needs sets up a presumption that it has. The court also held that accumulating earnings for the purpose of redeeming stock of shareholders is a reasonable business need where it’s necessary to guarantee the existence of the business or promote harmony in the operation of the business. If the accumulation is justified to be within the reasonable needs of the business, the iaet is not imposed.

Further reduced by amounts retained to cover the reasonable needs of the business (the “accumulated earnings credit”).7 purpose: The corporation could be subject to the personal holding company (phc) tax or the accumulated earnings tax, but it is not subject to both of them because phcs are exempt from the accumulated earnings tax. Workino caoital needs for ooeratina cvcle earnings retained to provide for working capital

This tax—added as a penalty to a company’s income tax liability—specifically applies to the company’s taxable income, less the deduction for dividends paid and a standard accumulated tax credit of $250,000 ($150,000 for personal service. Have been accumulated for the reasonable needs of the business or beyond such 'needs is dependent upon the particular circumstances of the case. When the revenues or profits are above this level, the firm will be subjected to accumulated earnings tax if they do not distribute the dividends to shareholders.

Corporate taxpayers that retain earnings in excess of the reasonable needs of their business rather than pay such earnings as dividends to shareholders are at risk for the accumulated earnings tax (aet), which is a form of penalty tax that is intended to make corporations distribute their taxable income to shareholders, rather than accumulate the income.

Income Tax Computation For Corporate Taxpayers Prepared By

Income Tax Computation For Corporate Taxpayers Prepared By

2

Improperly Accumulated Earnings - Mpcamaso Associates

/GettyImages-1130199515-b011f8c58a144789b22c7107929ffb8f.jpg)

Accumulated Earnings Tax Definition

Income Tax Computation Corporate Taxpayer 1 2 What Is A Corporation Corporation Is An Artificial Being Created By Law Having The Rights Of Succession - Ppt Download

Income Tax Computation Corporate Taxpayer 1 2 What Is A Corporation Corporation Is An Artificial Being Created By Law Having The Rights Of Succession - Ppt Download

So Be Iaet - Kpmg Philippines

Overview Of Improperly Accumulated Earnings Tax In The Philippines - Tax And Accounting Center Inc - Tax And Accounting Center Inc

Understanding The Accumulated Earnings Tax Before Switching To A C Corporation In 2019

Strategies For Avoiding The Accumulated Earnings Tax - Krd

Income Tax Computation For Corporate Taxpayers Prepared By

Irs Use Of Accumulated Earnings Tax May Increase

Income Tax Computation For Corporate Taxpayers Prepared By

Corporate Accumulation Penalty Taxes

Income Tax Computation For Corporate Taxpayers Prepared By

Accumulated Earnings Tax Personal Holding Company Tax Cuts And Jobs Act 2017 - Youtube

Income Tax Computation For Corporate Taxpayers Prepared By

Income Tax Computation Corporate Taxpayer 1 2 What Is A Corporation Corporation Is An Artificial Being Created By Law Having The Rights Of Succession - Ppt Download